I’m getting slightly annoyed with people telling me that the proclaimed dead live longer. Almost everyday you hear someone passing by that RIM is a good investment at this time. The problem is, that the prospects of RIM succeeding are highly uncertain. I’m sure they have an excellent team working across the street from my office (note: I work for UW), but the crystal ball looking ahead is more than blurred.

Wouldn’t it be nice if looking at today’s stock price of about 17$, you could have entered at say $10 or less?

In fact with a little derivative black magic you could achieve something similar, while keeping the value at risk manageable and at the same time get paid to buy RIM at a discount.

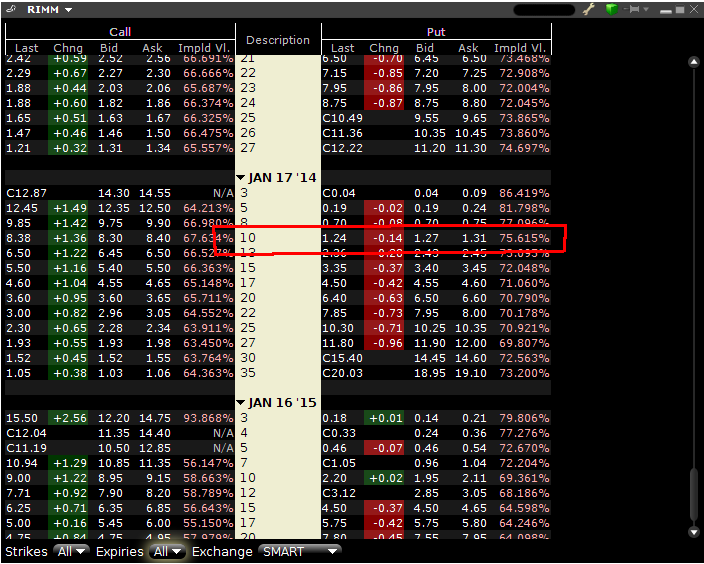

Looking at the RIM January 2014 Puts have an implied volatility of about 75% and require a premium of 1.24$. Here is a possible play (ignoring commissions for simplicity)

- Sell X x 10$ January 14 Puts short to open today

- Since option contracts cover 100 shares, you would receive X x 124$ for each put.

- Since the strike price is 10$, your value at risk is X x 1000$, or otherwise put

- Your yield on risk is about 12.4% (which is a pretty sweet deal compared to GICs)

In other words you would get paid 1.24$ to wait for RIM to fall back to $10. To explain the idea consider the following

potential outcomes in January 2014.

- Option 1: RIM stock is worth more than 10$, in that case the option that you sold short expires worthless. That means you keep your X x $124 regardless. You might have missed a bit on the upside, nevertheless you made 12.4% yield by risking just 1000$ for a year.

- Option 2: RIM stock is worth less than 10$ (or for that matter less than $8.76). Here you’ll still be happy compared to your neighbour or hairdresser that bought the stock today at 17$. By getting paid $1.24 per share by selling puts short, you would have offset your cost base down to $8.75. A potential fall from a cost-basis of $8.76 today to whatever happens in January will feel a lot less painful than a fall from $17 today.

I hope you’ve enjoyed this little excerpt of derivatives black magic. Do not attempt this approach if you have no idea how option markets work. Spend some time to learn the internal workings and pricing mechanisms first, before you jump into hot waters like this.

Disclosure: This is just an example calculation. I do not have a significant position in RIM right now. RIM is still too risky for me and big blow-ups like Nortel are still in my memories.

Crossposted from my old blog

Published: 2013-01-22

Updated : 2025-10-04

Not a spam bot? Want to leave comments or provide editorial guidance? Please click any

of the social links below and make an effort to connect. I promise I read all messages and

will respond at my choosing.